_Futurization

Authors: Johnettan Tokdemir, Insurance Expert & Ertan Sener, Insurance Expert

Every company wants to avoid the cancellation and loss of existing customers under all circumstances – and of course this also applies to the insurance industry. The problem is that, based on purchasing experiences at Amazon and the like, insurance policyholders expect individual services tailored to their needs and consistent customer communication across all channels. If insurers do not actively invest in the design of their customer journey in the future, they risk losing significant parts of their portfolios. The solution: with data-driven churn management, insurers can optimize their customer contact across channels and build long-term relationships with their customers. Let’s take a look at how insurers position themselves in churn management, and what starting points and scenarios there are for avoiding cancellations along the customer journey.

Churn management makes customer relationship management fit for the future

Short notice periods, increasing competition, comparable products: the risk of churn among existing customers is constantly increasing. It is therefore all the more important for the future economic security of insurers to reduce this risk with the help of sustainable churn management and to integrate this into an omnichannel strategy in the long term. Churn management helps to identify customers who are willing to switch and to carry out targeted countermeasures in good time to avoid cancellation. The aim is to identify customer needs through a high level of customer focus and automation, to respond to them early on to achieve a high level of customer satisfaction, and to retain existing customers in the long term. Churn management along the entire customer journey is essential for customer interaction in the future, especially taking into account the considerable acquisition costs for gaining new customers and the current difficult market climate for new acquisitions.

Customers considering canceling are 96% likely to do so.

Source: WAVESTONE survey

The probability that a customer will switch is indicated by an individual churn score, which is determined from data collected from all interactions along the customer journey. Basically, cancellation or migration can be attributed to the following factors:

Price makes the difference

Depending on the product and contract term, and also in view of constantly growing economic challenges, policyholders will either choose cheaper alternatives within an insurer’s offering (down-selling) or cancel. In particular, price-sensitive policyholders in high-fluctuation lines of business are increasingly taking this route.

It’s a match?

But maybe it just hasn’t “matched” between the policyholder and the insurer. Both the product and the identification of the respective customer group with the brand play a major role here. Due to the growing relevance of sustainability criteria, “matching” with the brand is increasingly becoming the focus of certain target groups.

It‘s all about Customer Experience

The customer experience begins with the potential customer’s first impression, and solidifies with every further interaction along the customer journey. This creates the opportunity and need to provide the most suitable customer experience at all times. Often, a minimal amount of personalization or room for understanding can make the difference in the customer relationship going forward.

Using churn prevention to strategically manage customer switching

Through targeted actions, insurers can influence the churn score of their policyholders across the following categories:

Incentives: With the help of discounts or other forms of monetary incentives, price-focused customers in particular can be retained. Combined with customer lifetime value, insurers can achieve long-term conversion and retention through short-term incentives.

Compensation: Actual customer centricity is achieved through the continuous integration of customer feedback within the framework of an open-error culture. If the customer has a negative experience during the customer journey, a positive signal effect in the form of monetary and non-monetary compensation can prevent possible switching. In this way, the customer acts as a central quality assurance for the insurer and enables constant improvement of the experience through direct feedback along each individual customer journey.

Communication: To increase transparency due to immateriality, open and barrier-free communication is essential. Along the customer journey, an insurer has various opportunities to exchange information. Personal communication with customers enables unbiased insights for the collection or direct management of the churn score. One possible approach is to explain to policyholders in a business transaction (for example in the claim notification) which information is requested and for what reason, or which information is not yet available in the process. Therefore, an insurer can increase acceptance in a customer journey with transparent communication about process weaknesses.

Barriers to churn: The loyalty of existing customers increases through the targeted promotion of cross-selling, up-selling and other measures for customer retention and therefore a higher contract density per policyholder. This can influence the churn score and reduce the likelihood of cancellation and switching.

To actively manage possible reasons for switching such as price, match and customer experience, data plays an essential role and provides important metrics such as customer lifetime value and churn score.

“Currently, most insurers focus on predicting cancellations. However, it is much more important to know how to actively avoid termination.”

Johnettan Tokdemir, Senior Manager and insurance expert at WAVESTONE

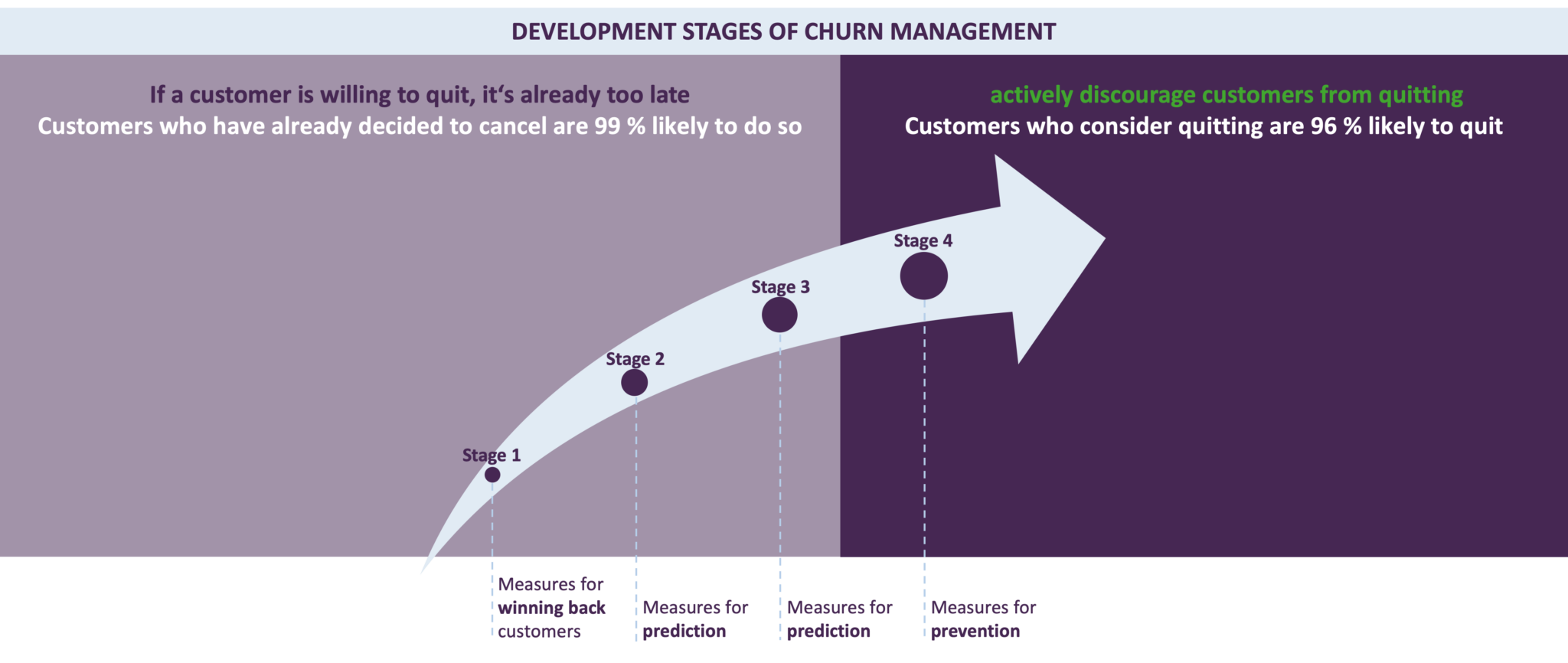

Four development stages can be identified among insurers regarding churn management

grafik_EN

The availability, preparation and use of customer-specific data forms the backbone of digital churn management. Basically, companies can be divided into four categories based on their stage of development. Most insurers still focus on customer recovery and prediction (stages 1 to 3). The bigger picture shows that long-term customer loyalty is primarily created through forward-looking behavior by insurers that is tailored to the customer. This is the aim of the fourth stage of development.

Stage 1: Measures to win back customers

This is classic customer recovery and therefore the insurer’s response to a cancellation that has already been submitted. Such measures largely involve analog components such as active customer contact by the managing agent to clarify the cause of the cancellation, and result in a very low success rate. A lack of structured data makes it difficult to implement a hyper-personalized process for responding to a cancellation in line with the customer’s needs, and reduces the already low chances of success in winning back customers.

Stage 2: Measures for prediction

The data available in the company enables the insurer to make initial predictions. The customers are segmented and a corresponding range of measures is available for each segment – the prediction focuses on cross-, up- and down-selling potential and not on cancellation. The sales department has access to all relevant information at all times and guarantees customers their personally preferred channel as a means of communication.

Stage 3: Measures for prediction

At this stage of development, there is a data basis extended to the customer ecosystem (including information on third-party providers). Customers are therefore transparent to the entire company and existing information can be used by the insurer to intervene with targeted measures in churn retention and churn prevention. Since each customer touchpoint is assigned a churn score, weak points along the customer journey can be quickly identified and cancellations can be reliably predicted.

Stage 4: Measures for prevention

In a holistically integrated infrastructure, all customer touchpoints with the insurer are tracked and evaluated. In doing so, the insurer enriches the customer data underlying the CRM with the information globally available on the customer (for example via Google Analytics). Using artificial intelligence, cancellation probabilities are calculated from the available information and, against this, individual retention measures (for example discounts and additional services) are automatically triggered to systematically address customer needs, and with data support. These measures and a positive customer journey ensure customers remain loyal to the insurer in the long term – even before they feel the need to continue their customer journey with a competitor.

Can “switchers” be stopped?

Individual initiatives in the insurance industry indicate that the need for intelligent churn management in existing customer business has been recognized. To remain competitive, existing churn models must be expanded in future to include individual measures for each customer cluster and reason for churn, and customer interactions must be evaluated along the customer journey. The challenge here is to add and further expand churn retention and churn prevention measures along an omnichannel strategy.

One thing is certain: if a policyholder is already considering canceling, there is a less than five percent chance this can be changed. Once the customer has started the symbolic journey and therefore the cancellation process, there is only one thing left for the insurance company – a final good impression in the form of a positive customer experience. To answer the question, “switchers” cannot be stopped – so insurers must successfully change from prediction to prevention with their future omnichannel strategy to actively respond to declining new business through existing customers.

Johnettan Tokdemir

Insurance expert

Johnettan Tokdemir is responsible for the Service Excellence topic area at WAVESTONE. With more than twelve years of expertise in the insurance and financial services industry, he has been able to build up in-depth knowledge in the area of customer centricity and automation. With his team, John Tokdemir successfully implements innovations around omnichannel strategies.

Ertan Sener

Insurance expert

Ertan Sener is a Senior Consultant at WAVESTONE and has been consulting in the Public Services, Utilities and Insurance sectors for almost 9 years. His focus is primarily on the topics of Customer Centricity and Customer Service Excellence. In the course of this, Ertan Sener is responsible for the data- and customer-centric development of digital services.

Together with you, we are rethinking the future of the insurance industry. Contact us for an initial exchange.